Mortgage Payoff Calculator: Pay Off Your Home Years Sooner

Paying off your mortgage early can save you tens of thousands of dollars in interest and shorten your loan term significantly. Use our Mortgage Payoff Calculator to see how making extra payments can accelerate your path to being completely debt-free.

New Payoff Date

--

Time Saved

--

Interest Saved

$0

Loan Balance Over Time

How to Use Our Mortgage Payoff Calculator

To find your new payoff date and total savings, you’ll need a few details from your latest mortgage statement.

Original Loan Amount: Enter the full, original amount of your mortgage loan in dollars. For example, if you borrowed $350,000, enter that amount.

Annual Interest Rate (%): This is the yearly interest rate on your loan, not the APR. You can find this on your statement.

Loan Term (Years): Select the original length of your mortgage, typically 30 or 15 years.

Loan Start Date: Enter the month and year your loan payments began. This helps us calculate your current balance and remaining term accurately.

Extra Monthly Payment: This is the key. Enter any amount you plan to pay in addition to your regular monthly mortgage payment. Even $100 per month can make a significant difference.

One-Time Lump Sum Payment: If you’ve received a bonus, inheritance, or other windfall, enter the amount here. The calculator will show you the impact of applying this single extra payment directly to your principal.

Understanding Your Results

The most exciting numbers our calculator provides are your New Payoff Date and your Total Interest Savings. But what do they really mean? It all comes down to principal and interest.

When you make your standard monthly payment, a large portion initially goes toward interest, and a smaller portion goes to your principal (the actual loan balance). Over time, this slowly shifts.

An extra payment changes the game. 100% of your extra payment is applied directly to the principal. This has two powerful effects:

Reduces Future Interest: By lowering the principal balance faster, you reduce the amount of interest that can be charged on that balance in all future months.

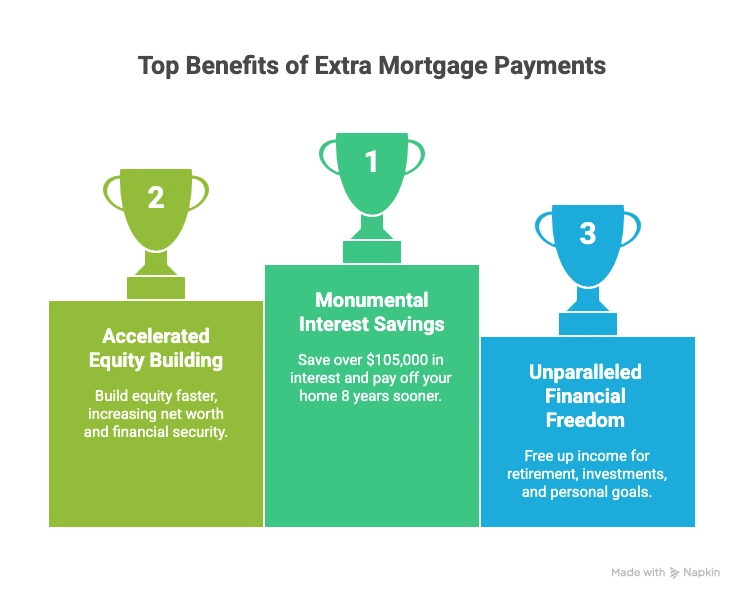

Accelerates Equity: You build equity in your home much more quickly, moving you closer to full ownership.

The results section will show you a side-by-side comparison. Here’s an example of what you might see for a $300,000 loan with an extra $250 per month payment:

| Metric | Original Loan (30-Year Fixed) | With Extra $250/Month | Your Savings |

| Payoff Date | July 2055 | April 2049 | 6 years, 3 months sooner |

| Total Interest Paid | $347,225 | $281,450 | $65,775 Saved |

| Total Amount Paid | $647,225 | $581,450 | $65,775 Saved |

We also recommend visualizing your results with a chart showing how your loan balance decreases over time. The “With Extra Payments” line will show a much steeper decline, hitting zero years sooner.

(A line chart showing two curves—”Original Balance Over Time” and “Balance With Extra Payments”—would be placed here.)

Frequently Asked Questions

Is it always a good idea to pay off my mortgage early?

For most people, paying off a mortgage early is a financially sound goal that provides peace of mind and significant interest savings. However, there is an “opportunity cost” to consider. If your mortgage interest rate is very low (e.g., 2.5% – 3.5%), you might potentially earn a higher return by investing that extra money in the stock market or contributing more to a tax-advantaged retirement account like a 401(k) or IRA. The best choice depends on your personal risk tolerance and financial goals.

How do I ensure my extra payment is applied to the principal?

This is a critical step. Simply including extra money in your check might cause the lender to hold it and apply it to your next month’s payment (interest and all). To avoid this, you must explicitly instruct your lender to apply the additional funds “directly to principal.” Most online payment portals have a specific box for “extra principal payment.” If you pay by mail, write “For Principal Reduction Only” and your loan number in the memo line of your check. It’s wise to check your statement the following month to confirm it was applied correctly.

Is it better to make extra monthly payments or one large lump-sum payment?

Both methods are effective, but they serve different scenarios.

Extra Monthly Payments: This strategy is great for building a consistent habit. It’s systematic and allows you to chip away at the principal steadily over time, often without drastically changing your budget.

Lump-Sum Payment: This is ideal if you receive a sudden influx of cash (e.g., a work bonus, inheritance, or tax refund). A single large payment can shave years off your loan and save a substantial amount of interest instantly.

Our calculator allows you to model both scenarios to see which one aligns better with your financial situation.

What about bi-weekly payments? Do they help pay off a mortgage faster?

Bi-weekly payment plans work by having you pay half of your monthly mortgage payment every two weeks. Because there are 52 weeks in a year, this results in 26 half-payments, which is equivalent to 13 full monthly payments per year instead of the standard 12. That one extra payment per year is what accelerates your payoff. You can achieve the exact same result by simply dividing your monthly payment by 12 and adding that amount to your principal each month—without needing a third-party service that may charge a fee.

How much faster can I pay off my mortgage with an extra $200 per month?

Let’s use a concrete example. Imagine you have a $350,000, 30-year mortgage that you started 2 years ago at a 6.0% interest rate. Your regular monthly payment for principal and interest is approximately $2,098.

Original Plan: You would pay a total of $405,420 in interest over 30 years.

With an extra $200/month:

You would pay off your mortgage in 23 years and 10 months instead of 30 years.

You would pay only $301,650 in interest.

This simple change saves you $103,770 and gets you out of debt more than 6 years sooner.

Are there prepayment penalties I should worry about?

Prepayment penalties are fees some lenders charge if you pay off all or part of your loan too early. While they became less common after the 2008 financial crisis, they still exist, particularly with certain types of loans. Before sending any extra payments, check your original loan documents or call your lender and ask directly: “Does my loan have a prepayment penalty?” This simple check can save you from an unwelcome surprise.

Take the Next Step in Your Financial Planning

Now that you’ve seen how to pay off your mortgage faster, you can explore other ways to strengthen your financial position.

If your current interest rate is high, use our Refinance Calculator to see if you can lower your monthly payment and overall interest costs.

Want to see a full payment-by-payment breakdown of your loan? Dive into the details with our Amortization Schedule Calculator.

Creator