Retirement Calculator: Are You Saving Enough?

Answering the question, “Will I have enough money to retire?” is the foundation of a secure financial future. This retirement calculator helps you see where you stand by projecting your savings growth and estimating if you’re on track to meet your retirement income goals.

Retirement Savings Analysis

After retirement (if saved ):

After retirement (if saved ):

How can you save ?

Savings Plan Results

If you save every month until 67

If you save every year until 67

If you have it now

Balance at retirement age of :

Equivalent to current purchase power of:

If withdraw at fixed purchasing power amount

If withdraw at fixed amount

The following are some other withdraw amount/length schedules.

| Withdraw Length | Withdraw Amount |

|---|

How to Use Our Retirement Calculator

Provide the following details to get a personalized snapshot of your retirement outlook. Each field plays a key role in the final calculation.

Current Age: Enter your age today. This sets the starting point for your retirement savings timeline.

Retirement Age: Enter the age at which you plan to retire. The difference between this and your current age is your investment horizon—the time your money has to grow.

Current Retirement Savings: Input the total amount you have already saved for retirement across all accounts (e.g., 401(k), IRA, brokerage accounts).

Monthly Contribution: Enter the total amount you are currently saving for retirement each month. Be sure to include both your personal contributions and any employer match you receive.

Rate of Return (Pre-Retirement): This is the estimated annual percentage return you expect your investments to earn before you retire. A common long-term estimate for a diversified stock portfolio is between 6% and 8%, but you can adjust this based on your risk tolerance and investment strategy.

Rate of Return (Post-Retirement): Enter the estimated annual return you expect your investments to earn after you retire. This is typically a more conservative number (e.g., 3-5%) as your portfolio shifts from growth to preservation.

Desired Annual Income (in Retirement): How much money do you want to live on per year in retirement? A common guideline is to aim for 80% of your pre-retirement income, but you can adjust this based on your expected lifestyle.

Understanding Your Results

The calculator provides a powerful projection of your financial future. The results show you two critical pieces of information: your total estimated savings at retirement and whether you are on track to fund your desired lifestyle.

Your Retirement Nest Egg: A Breakdown of Growth

The final savings number isn’t just the money you put in; it’s the result of your contributions working together with the power of compound growth.

| Component | Description |

| Total Contributions | This is the sum of all the money you (and your employer) will have put into your accounts from now until retirement. |

| Total Investment Growth | This is the “magic” of compounding. It’s the money your money earns over time. The longer your timeline, the more significant this portion becomes. |

| Estimated Nest Egg | This is the grand total at retirement—the sum of your current savings, all future contributions, and all investment growth. |

Ending Balance

$0

Total Contributions

$0

Total Investment Growth

$0

Are You on Track? Shortfall vs. Surplus

The calculator compares your estimated nest egg to the amount needed to generate your desired annual income throughout retirement.

Retirement Surplus: If the results show a surplus, it means your projected nest egg is more than enough to support your desired retirement income. You are on the right track.

Retirement Shortfall: If the results show a shortfall, your current strategy is not projected to be enough to meet your goals. This is not a reason to panic; it’s a signal to take action. The calculator will show you exactly how much more you need to save to close the gap.

Frequently Asked Questions

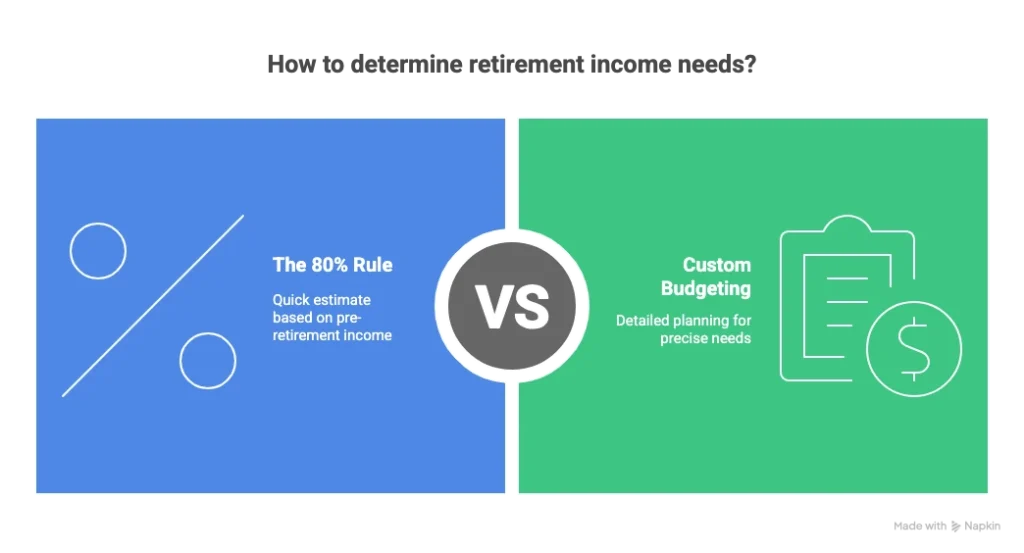

How much money do I really need to retire?

While the old “million-dollar” rule of thumb is popular, the real answer is highly personal. It depends entirely on your desired lifestyle in retirement. A more effective method is the “80% Rule,” which suggests you’ll need about 80% of your pre-retirement annual income to maintain your standard of living. For example, if you earn $80,000 per year before retiring, you should plan for about $64,000 per year in retirement income. Another approach is the “4% Rule,” which suggests you need a nest egg 25 times your desired annual income.

Concrete Example: You want $60,000 per year in retirement income. Using the 4% Rule: $60,000 x 25 = $1,500,000. You would need an estimated $1.5 million saved to safely withdraw $60,000 per year.

What is a “safe withdrawal rate”?

A safe withdrawal rate is the percentage of your retirement savings you can withdraw each year without running out of money. The “4% Rule” is the most common guideline. It states that you can withdraw 4% of your starting nest egg in your first year of retirement and then adjust that amount for inflation each subsequent year. This strategy has historically been shown to have a high probability of success over a 30-year retirement. The rate you choose for the “Rate of Return (Post-Retirement)” field in the calculator reflects the investment returns you’ll need to sustain these withdrawals.

What should I do if the calculator shows a shortfall?

Seeing a retirement shortfall is the first step toward fixing it. You have several levers you can pull:

Increase Your Monthly Contribution: Even small increases can make a huge difference over time due to compounding.

Delay Retirement: Working just a few extra years gives your money more time to grow and reduces the number of years you’ll need to draw from your savings.

Adjust Your Expected Rate of Return: This could mean re-evaluating your investment strategy to take on slightly more risk (if appropriate for your age and risk tolerance) for potentially higher returns.

Lower Your Desired Retirement Income: Re-evaluating your expected retirement budget might reveal areas where you can spend less.

What’s the difference between a 401(k) and an IRA?

Both are retirement savings accounts with tax advantages, but they have key differences.

401(k): An employer-sponsored plan. Contributions are often made pre-tax, lowering your taxable income today. Many employers offer a matching contribution, which is essentially free money. Investment options are limited to what the plan offers.

IRA (Individual Retirement Arrangement): An account you open on your own. A Traditional IRA may offer a tax deduction now, with taxes paid on withdrawals in retirement. A Roth IRA is funded with after-tax dollars, meaning contributions aren’t deductible, but all qualified withdrawals in retirement are 100% tax-free. IRAs offer nearly limitless investment choices.

How does inflation affect my retirement savings?

Inflation is the rate at which the cost of living increases, reducing the purchasing power of your money. A 3% inflation rate means that $100 today will only buy you $97 worth of goods and services next year. Your retirement plan must account for this. Your investment returns need to outpace inflation just to maintain your purchasing power. This is why a “Rate of Return” of 6-8% is often targeted—if inflation is 3%, your “real” return is only 3-5%. Our calculator factors this in implicitly when determining if your nest egg can support your income goal over a long retirement.

After using this calculator, you might want to dive deeper into specific aspects of your plan. Use our 401(k) Calculator to see how you can maximize your employer match, or explore different scenarios with our Investment Calculator to better understand potential rates of return.

Creator