Refinance Calculator with Closing Costs & Break-Even Point

Refinancing your mortgage could lower your monthly payment and save you thousands in interest, but it isn’t the right move for everyone. Our refinance calculator helps you compare your current loan to a new one and calculates your break-even point to see if a refinance makes financial sense for you.

Monthly Payment Savings

$0

Breakeven Point

--

Lifetime Savings

$0

Cumulative Savings Over Time

How to Use Our Refinance Calculator

To analyze a potential refinance, you’ll need details on both your current loan and the new loan you’re considering.

Your Current Mortgage

Current Loan Balance: Enter the exact amount you still owe on your mortgage. You can find this on your most recent mortgage statement or by logging into your lender’s online portal.

Current Interest Rate (%): Your existing mortgage’s annual interest rate.

Current Monthly Payment ($): Enter your current monthly payment for principal and interest only. Do not include amounts for property taxes or homeowners insurance (escrow), as these will not change with a refinance.

Your New Loan

New Interest Rate (%): The interest rate you have been quoted for a new loan. As of July 22, 2025, rates can vary, so getting a current quote is best.

New Loan Term (in years): The length of the new loan you are considering. Common options are 30, 20, and 15 years.

Closing Costs ($): The estimated total cost to close your new loan. This typically ranges from

2%to5%of the new loan amount and includes fees for the appraisal, title search, and lender processing. You can get an estimate from your potential lender on a Loan Estimate document.

Is Refinancing Worth It? Understanding Your Results

Our calculator provides three key outputs to help you make an informed decision.

New Monthly Payment: This is the new principal and interest payment for your refinanced loan. This shows you the immediate impact on your monthly cash flow.

Total Monthly Savings: This is the direct, dollar-amount reduction in your monthly payment. While a lower payment is appealing, this number alone doesn’t tell the whole story.

Your Break-Even Point: This is the single most important result. It tells you how many months it will take for your monthly savings to pay for the closing costs of the refinance. The formula is:

Break−Even Point (in months)=Monthly SavingsClosing CostsIf you plan to stay in your home for longer than the break-even period, the refinance will likely save you money in the long run.

Loan Comparison Example

| Metric | Current Loan | Proposed New Loan |

| Loan Balance | $250,000 | $250,000 |

| Interest Rate | 6.5% | 5.5% |

| Monthly P&I | $1,580 | $1,419 |

| Closing Costs | N/A | $5,000 |

| Monthly Savings | $161 | |

| Break-Even Point | 31 Months |

In this scenario, it would take 31 months of savings to recoup the $5,000 in closing costs. If you plan to sell the home in two years, refinancing would be a loss. If you plan to stay for five years, it would be a clear financial win.

Frequently Asked Questions About Refinancing

When does it make sense to refinance?

Homeowners in the United States typically refinance for one of four reasons:

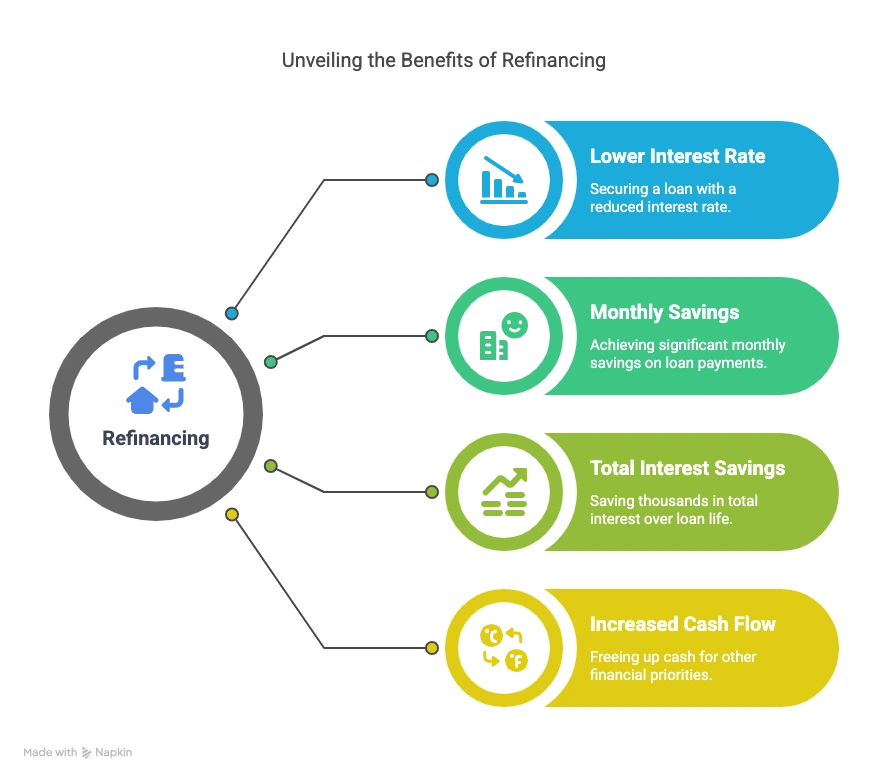

To Get a Lower Interest Rate: This is the most common reason. If market rates have dropped since you got your loan, you can lower your monthly payment and total interest paid.

To Shorten the Loan Term: If your income has increased, you might refinance from a 30-year loan to a 15-year loan. Your payment will likely increase, but you’ll pay off the home decades sooner and save a massive amount in interest.

To Convert an ARM to a Fixed-Rate Loan: If you have an Adjustable-Rate Mortgage (ARM) and are worried about future rate increases, you can refinance into the stability of a fixed-rate mortgage.

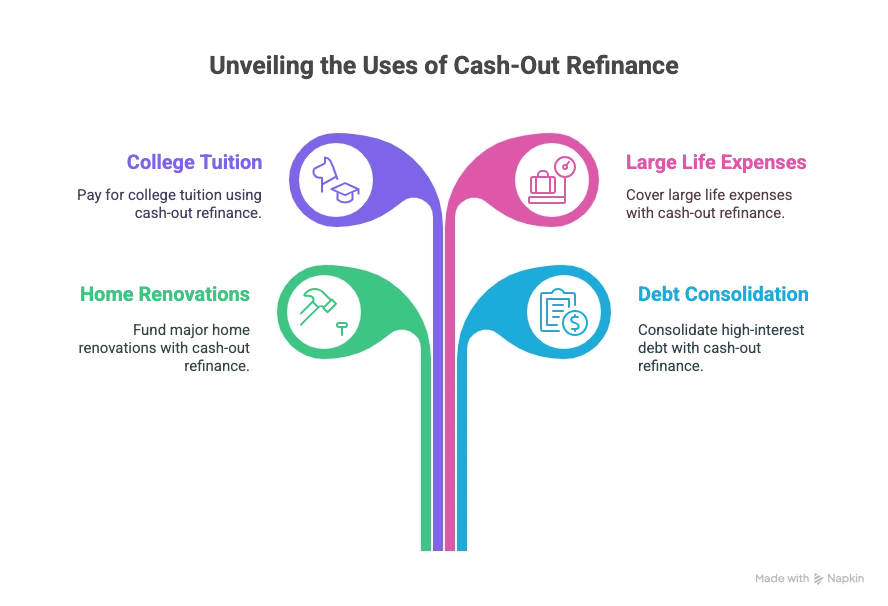

To Cash-Out Home Equity: A “cash-out” refinance allows you to borrow more than you owe and take the difference in cash, often used for home improvements, debt consolidation, or other large expenses.

What is a “no-cost” refinance?

Be very skeptical of “no-cost” refinance offers. The closing costs, which can be thousands of dollars, don’t just disappear. Instead, the lender handles them in one of two ways:

They are added to your loan balance: You borrow more money to cover the costs, meaning you pay interest on them for the life of the loan.

You accept a higher interest rate: The lender gives you a rate that is

0.25%or0.5%higher than the best available rate, and uses the extra profit to pay the closing costs on your behalf. There is always a cost.

Will refinancing restart my mortgage “clock”?

Yes, and this is a critical downside to consider. When you refinance, you are taking out a brand new loan with its own term. Concrete Example: Let’s say you are 5 years into a 30-year mortgage. If you refinance into a new 30-year loan to get a lower payment, your total repayment period will be 35 years (5 old + 30 new). While your monthly payment might be lower, you could end up paying more in total interest. To avoid this, consider refinancing to a shorter term, like a 20-year or 15-year loan.

What credit score do I need to refinance?

Lender requirements are very similar to when you first purchased your home. For a conventional refinance, most lenders look for a minimum credit score of 620. However, to qualify for the best-advertised interest rates, you will likely need a score of 740 or higher. A lower credit score will typically result in a higher interest rate, which may make the refinance less beneficial.

How much lower does my new rate need to be?

The old rule of thumb was to wait for a 1% or 2% rate drop, but this is outdated. The better approach is to use this calculator and focus on the break-even point. On a large loan, even a 0.5% rate reduction can save you significant money and result in a reasonable break-even period. The decision depends entirely on your loan size, the closing costs, and how long you plan to stay in the home.

Next Steps & Other Tools

Refinancing is a powerful tool when used correctly. Explore these other calculators to manage your mortgage and home equity.

If your primary goal is to pay off your mortgage faster, see how extra payments could accelerate your timeline with our Mortgage Payoff Calculator.

Considering a cash-out refinance for a home renovation or to consolidate debt? First, estimate your available equity with our Home Equity Calculator.

Want to see the full payment-by-payment schedule of your potential new loan? Visualize the breakdown of principal and interest with our Loan Amortization Calculator.

Creator